Your Credit Card Processor Raised Your Rates - Now What?

You know the drill. Your monthly credit card processing statement arrives in the mail, and your processor has increased your rates and fees. How do you stop it?

Credit card processing isn’t cheap. But it doesn’t have to be as expensive as many business owners think. In this post, we will cover the different types of price increases, which ones are avoidable, and how to stop them.

Types of Price Increases

When your processing rates go up, it could be because Visa and Mastercard has increased interchange rates, your processor increased their rates, or both.

When Visa and Mastercard increase the interchange rates, there’s nothing you (or your processor) can do to lower them again. However, processor rate increases are avoidable.

Determine the Source of the Increase

In credit card processing, a rate or fee increase can be the result of a few different things, some of which are in your processors control and some of which are not. You’ll need to first determine if the increase was your processor’s doing, or Visa and Mastercard’s doing.

Visa and Mastercard may increase interchange rates or assessment fees. If they do, there’s nothing your processor can do to lower those fees. However, your processor could add to it, making it a greater increase than necessary.

If Visa and Mastercard raised fees, you’ll need to confirm that you’re receiving the increases AT COST, without additional mark-ups. To do that, you can compare your interchange rates from a monthly statement to Visa’s and Mastercard’s published interchange rates.

Keep in mind that there’s no standardization to interchange category descriptions in processing statements. What Visa or Mastercard call an interchange category might not be how your processor lists it on your statement.

Is it true that my processor didn’t raise the rates, Visa and Mastercard did?

Processors may tell you that your processing costs went up because Visa and Mastercard raised pricing.

This is sometimes the case, but not always!

Keep in mind that your processor will include notices about price icnreases on your monthly statement. In some cases, the notice will simply state an impending rate change. In other cases, it may list the interchange categories and rates that changed.

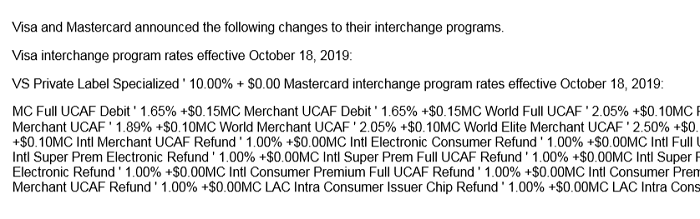

For example, here’s a statement that lists interchange rate increases from the card brands that occurred in October 2019. (Statement has been enlarged, not all categories shown.)

However, even when Visa and Mastercard do increase interchange rates, processors may raise your pricing more than Visa / Mastercard did.

To understand how that happens, it’s important to understand the different rates and fees that make up your total processing cost.

Parts of Processing Fees

We’ve covered the components of processing costs thoroughly in our previous post about credit card processing rates and fees, but for a quick recap:

Interchange: Typically, the largest part of processing costs. Interchange fees go to the banks that issue cards to your customers.

Assessments: Fees that go to the card brands (Visa, Mastercard, Discover) themselves.

Markup: The rates and fees that go back to your processor as their profit from your account.

When your processor charges you for processing, it includes all three of these components in one way or another. It may list them separately or bundled together, but all three pieces are always part of the total cost.

There are hundreds of different interchange “categories” but the rates are almost always a percentage and a cents fee. (E.g. 1.65% + $0.10.) Several assessments can apply to a single transaction. Assessments include both percentages and cents fees.

Your processor doesn’t control interchange or assessments. If Visa decides to raise its interchange fees, your processor can’t do anything about that. The processor will pass along the fee increase to you.

The processor only controls their markup, which is in addition to interchange and assessments. They can charge a percentage, cents fees, monthly fees, or some combination. Most processors charge a combination, but there are exceptions.

For example, subscription-style processors like Payment Depot charge 0% markup, but have higher cents fees and monthly “subscription” fees.

So, when Visa or Mastercard raise the interchange rates or assessment fees, your costs do go up and your processor doesn’t control that. However, what the processor does control is whether it passes the increase to you at cost or if it “pads” the fee, and whether it raises its own part of the rates, i.e. the markup, at the same time.

Additionally, your processor can raise your markup at any point even if Visa and Mastercard don’t raise their rates.

Ending Price Increases

You can’t completely eliminate increases in processing costs. When Visa and Mastercard raise rates, your costs will go up. However, what you CAN do is make sure that your costs only go up as much as Visa and Mastercard say. In other words, you can eliminate the unnecessary processor markup increases and sneaky interchange padding.

How? Secure true pass-through pricing and a lifetime rate lock.

At Tailored Transactions, that is exactly what we will provide to your business. We will setup your merchant account with TRUE Cost-Plus Pricing with a guaranteed lifetime rate lock. Meaning that the processing rates and fees that we charge to you will NEVER be increased for the life of your account with us.

Also, we will always pass-through interchange rate increases at COST with no additional markups!

Have additional questions? Want to receive a no-obligation Free Rate Quote for your merchant services?

Visit us online at www.TailoredTransactions.com or call us direct at (888) 669.1686